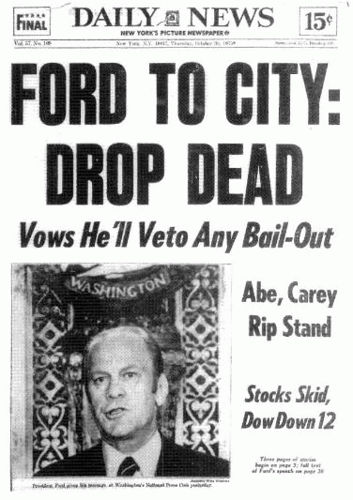

It seems like Déjà vu all over again. Back in the 1970's we were in a war that would not end, President Nixon had been deposed, the American automobile industry was reeling, gas prices were making us change our driving habits and lifestyles, the stock market was in turmoil, President Ford was defiant over his pardon of Nixon and refusal to bail out NYC, foreclosures were up, and hope was down.

After we exited Viet Nam, I think everyone breathed a collective sigh of relief. Our terrible nightmare was over. We vowed "Never Again" and meant it. In 1976 the Democrats won both the Senate and House, many statehouses and governorships, and the big prize: The Presidency. Jimmy Carter took over and had his honeymoon with Congress and the public.

Fast forward 32 years. We are no longer fear the Commies. Now we fear terrorists. And rightly so.

The 1980's and 1990's were good for a lot of Americans. Reagan made most of the public feel good, even if they didn't agree with his policies. The Berlin Wall fell, Communism failed, the Baby Boomers made money in the stock market, the middle class went on a spending spree, and life was great once again. But September 11th changed all of that.

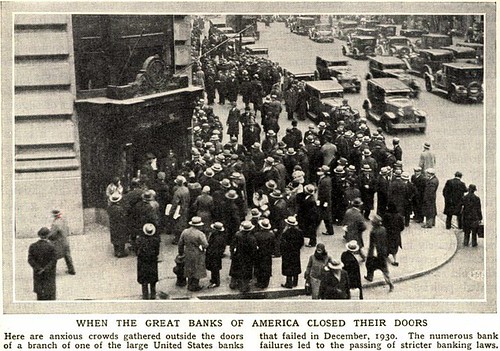

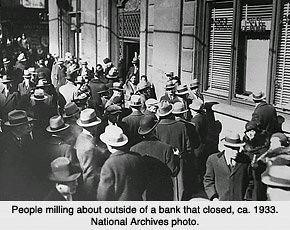

Our economy is in worse shape now than it was 30 years ago. The cost of fuel keeps going up, the price of groceries goes up or the size of packages shrink, American icons such as Anheuser-Busch and The Chrysler Building get sold to foreign entities, the threat of possible bank closings looms, and the housing crisis just gets worse. As the Baby Boomers approach retirement it looks like Social Security may not be as secure or as helpful as we once thought. It is not the Economy Stupid. It is the Stupid Economy.

There are a lot of busy Realtors in Key West this summer. We are all working with people who want deals. We send e-mails of new listings to prospective buyers who tell us what they want and what they are willing to pay. We drive them around town showing properties. Some people end up buying. Most express fear that prices will drop more and go back home hoping they do.

A real estate investor who owns a variety of income producing properties recently lowered the asking price on several. Several months after Hurricane Wilma, my client made an offer to purchase a commercial property the investor owned. The property was not used since Wilma. The owner bought the property in 2004. But his asking price was a $900,000 more than he paid for it. In early 2007 my buyer offered about $400,000 over the price the investor paid for the property. The investor said no deal. Earlier this year my buyer offered about $300,000 over the amount the investor paid. No go. Earlier this week, my buyer offered about $75,000 under what the investor paid. My buyer said "He should have accepted my price when I made it two years ago." My buyer is very pessimistic about the economy in general. He has cash in the bank and can buy without borrowing money. But he is reluctant to buy in the current market. He is fearful it will get worse. I understand.

We recovered after Nixon-Ford-Carter went away. We are going to have a new President in January. Bush will be history. I think the whole world will breath a very loud sigh of relief. And things will get better. I'm pretty sure all markets will re-bound right after the Inauguration. They may even pick up before the election. And when the rebound starts, it might just shoot up like crazy. Not everybody is poor and desperate. There are a lot of people waiting in the wings ready to buy. They just have to get over the Fear Factor.

If you think I'm full of beans, consider what Warren Buffet has to say about Market Timing: "Investors should remember that excitement and expenses are their enemies. And if they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful."

CLICK HERE to checkout the Key West Association of Realtors mls database of all current listings. If you see something you like please call me, Gary Thomas, 305-766-2642 or e-mail me at kw1101v@aol.com.

{kind=link}

{kind=link}

{kind=link}