I discovered Mad Men a couple of weeks ago. It is an AMC Cable TV series that is executive produced by Scott Hornbacher (The Sopranos). The first season of Mad Men takes place in the year 1960, and you can watch every episode if you have On Demand on your cable. Spend an afternoon or two and invest in some good TV if you have not watched it.

The sets, the furniture, the lamps and artwork, the cars, the clothes, the hair styles and hair cuts, the incessant chain smoking, the expense account lunches, and the martini drinking transport us back to a kinder, gentler time. Forty-eight years later those of us who lived through that time can look back, not in anger, but with nostalgia, and remember how much easier life was then.

In one of the first episodes Betty was shopping in the grocery store. Vintage products whose brands have disappeared or whose logos have changed remind us of things we have long forgot. In the vegetable aisle we see prices that look like food was almost free by comparison to today's prices.

The interior shots of the characters' homes look so dated. Betty Draper, the wife of Don (Juan) Draper (the male lead) looks like Betty Furness in her 1960's kitchen complete with knotty pine walls. Some of the rooms look like some houses I occasionally show in the New Town area of Key West, except people still live in those houses--houses that were built and furnished in the 1960s and not updated except for maybe a plasma TV or computer. And the Key West version is nowhere nearly as swank.

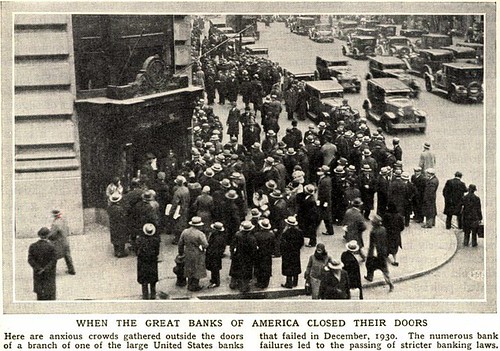

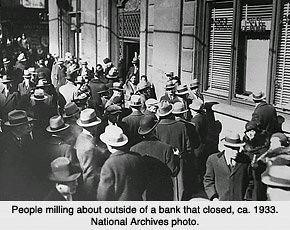

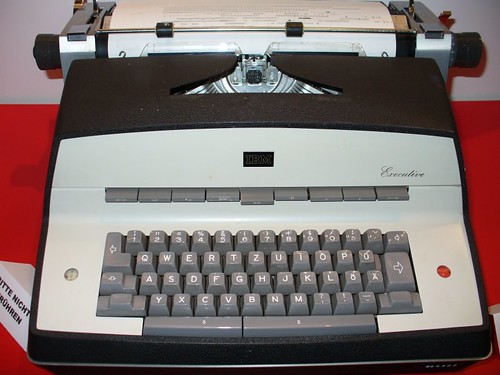

Later we see the corporate office with the IBM Executive Typewriters and other almost antique office furniture and fixtures. But it is when ad exec Pete Campbell states his salary is $75 per week salary that we are shocked into 21st Century reality. Seventy-five dollars! Per Week! In one of the last episodes Peggy Olsen gets elevated from secretary to junior copywriter and a salary of $35 per week. That is a time when most women were relegated to being either homemakers or the servants to men in the workplace. That is pre-glass ceiling. And pre-civil rights as well. Not a black to be seen in the office except a janitor who gets to spy a sexual romp through the opaque glass of an adman's office.

Later we see Pete Campbell and his wife Trudy go shopping for a Manhattan apartment that was offered at $30,000. Now I realize this is TV and that the apartment is a set, but CLICK HERE this is how much you could buy in 1960's New York for thirty grand. Most cars cost that much these days.

I was 13 in 1960. I remember it quite well in some respects. I remember that you could buy a regular Coke for a nickel and a King Sized Coke for a dime. McDonalds was new to Denver, and you could buy a hamburger for 15 cents, fries and a Coke for a dime each. I could eat a nice lunch for about fifty cents--the original Value Meal. There used to be roadside truck stands where my mom would by fresh farm produce in the summer. I remember Rocky Ford Cantaloupes and ripe watermelons for about a nickel a pound. And gas cost about 20 cents per gallon for as long as I could remember. I have some old black and white movies my uncle took of a Skelly Gas station he owned on Speer Boulevard in Denver in the 1940s. Gas cost 15 cents back then. Twenty years later it cost 20 cents per gallon. Almost 50 years later it costs about $4.35 per gallon.

Everything was cheaper back in the 1960s. As I recall most of the people I knew had one car and one TV. I don't remember any of my friends wearing a designer anything. Haircuts cost a buck and we all looked well fed and well bred.

I seem to recall the first minimum wage job I had paid $1.00 per hour in the mid 1960s. Then the minimum went up to $1.10. Man, I was rich with the stroke of a pen.

I remember my parents looked at buying a new house in the Applewood area 10 miles west of Denver in the early 1960s. I recall it cost about $15,000. I just looked at some similar houses online and they are now being offered in the $400,000s to $500,000s.

The cost of everything has gone up since the "Mad" 1960s. I don't have any idea what a Madison Avenue ad executive makes today, but I'll wager it is a lot more than the $75 per week Pete Campbell ad exec made. I know that today an apartment in Manhattan costs way more than $30,000. I would guesstimate that most shop clerk type jobs pay about $10 - $16 per hour in Key West. Most hard labor jobs pay between $17 to $25. Carpenters get paid $45 to $65 per hour in Key West. A studio apartment in Key West costs about $1100 per month. A one bedroom apartment in Key West would cost $1200 per month or more. And a buyer can probably pick up a nice two story town house at the Key West Golf Club for under $300,000.

The simple life of the 1960s is gone. Today many families have a car for every person of driving age, a TV in every room, and a cell phone for each family member capable of using one. Many families own at least one vacation home in addition to the family residence. We have so many things that have made our lives less simple.

Inflation has made the cost of many things seem terribly high, but the cost of some things we use daily have become so cheap that they are now considered disposable instead of repairable: TVs, cellphones, computers, major appliances, gas blowers, etc. You get the idea. I know that there are some people who read my little blog that think the cost of houses in Key West is still too high. I think that prices have moderated quite a bit. There are still some mis-guided missiles in the Key West real estate market who continue to over-price their listings. But there are probably as many bottom-feeder buyers trying to suck the smell off of every zero in a real estate contract.

Invest some of your time and watch Mad Men on AMC. See how much better (or worse) our lives are nearly a half century later. If you think the next half century will bring us equally good fortune, you might be interested in buying a house in Key West at some of the best prices in a long time. CLICK HERE to checkout the Key West Association of Realtors mls database of residential and commercial listings. If you see something you like please call me, Gary Thomas, 305-766-2642 or e-mail me at kw1101v@aol.com.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}